In the 13th installment, we focus on the European Free Trade Association.

Economic Background

In a world of trade blocs that span entire continents, the European Free Trade Association (EFTA) probably isn’t the most prominent organization of its kind. It is, however, one of the oldest in the world, and its small but wealthy members are constantly seeking new trade deals to bolster their export-based economies.

In 1960, the EFTA emerged as an alternative for countries that did not wish to join the European Economic Community, the European Union’s predecessor. The new bloc, led by the United Kingdom, was part of London’s strategy to carve out its own sphere of influence on the Continent, just as France and Germany had done with their rival organization. But over time, most of the EFTA’s original members — Austria, Denmark, Portugal, Sweden and, eventually, the United Kingdom itself — left to join the European Union. Of the bloc’s founders, only Norway and Switzerland stayed behind. Iceland joined their lonely ranks in 1970, followed by Liechtenstein in 1991.

Today, the EFTA is closely linked to the European Union because its members (except Switzerland) all belong to the European Economic Area, through which goods, people, services and capital move freely. (By contrast, hundreds of bilateral agreements govern Switzerland’s relationship with the European Union.) Nevertheless, the members of the EFTA stand apart from their EU peers in several important ways. For one, EFTA members do not contribute to EU agricultural subsidies or share their fishing areas with EU states. For another, they are not part of the eurozone, nor are they expected to join it in the future. But most important, they do not belong to the EU Customs Union, giving them the leeway to sign free trade agreements — both individually and collectively — with countries outside the larger Continental bloc.

Trade Implications

Trade Strategy

The EFTA’s members all possess small economies that depend on exports to maintain the high standards of living their people have come to expect. This is why, despite having only four signatories and a combined population of around 14 million, the bloc is the world’s ninth-largest trader in goods and fifth-largest trader in services. The EFTA also keeps a trade surplus: In 2016, its total exports exceeded 277 billion euros (a little over $322 billion), while its imports were valued at around 229 billion euros. Because its members are free to decide their own trade policies, the bloc isn’t as constrained by the diverging interests of its participants as is the European Union; instead it can be more flexible in trade negotiations. But this flexibility has its limits: EFTA countries are required to follow EU rules regarding issues such as technical barriers to trade, sanitary and phytosanitary measures, public procurement, and competition.

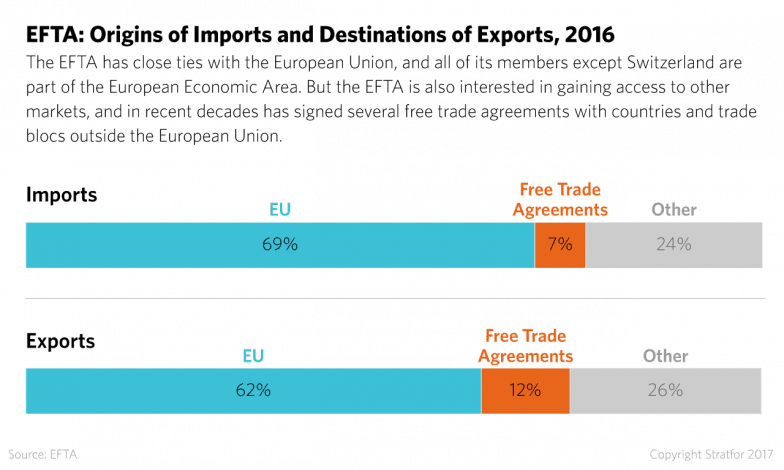

The European Union is easily the EFTA’s biggest trade partner. The larger bloc accounts for 60 percent of the EFTA’s exports and 70 percent of its imports. However, the EFTA has grander ambitions and hopes to gain access to other markets, often mirroring the European Union’s own attempts to do the same. As was true of its bigger peer, the EFTA began to get traction in its effort to build a wider trade network in the 1990s, when it adapted its approach to account for the challenges that globalization had spawned. And like the European Union, it sought out trade deals with former communist countries in Central and Eastern Europe, eventually extending its search to the Middle East and North Africa. By the mid-2000s, the EFTA had sent feelers across the Atlantic Ocean and into Asia. The new trade deals these efforts yielded ensured that by 2016, about 12 percent of the EFTA’s exports went to countries with which it had free trade agreements, while 7 percent of its imports came from them. And though the EFTA, fearful of losing ground to its Continental competitor, often mirrors the European Union’s strategy, its members are certainly free to make their own trade decisions. Unlike the European Union, for instance, Iceland and Switzerland have both signed free trade agreements with China.

Nevertheless, like the European Union, the EFTA will face several formidable challenges in the coming years. The first is to cope with membership turnover as some states leave the bloc and others join it, altering the balance of power and collection of interests within the organization. For example, Iceland submitted an application for EU membership in 2009. Though the island nation withdrew its bid in 2015, its departure would have trimmed the ranks of the EFTA to three, raising questions about its future. Accepting new members could prove equally problematic, particularly in the case of large economies whose entrance would doubtless disrupt the status quo. The United Kingdom isn’t currently considering EFTA membership, but that may not be the case forever. And any other countries that leave the European Union in the future may not share its disinterest.

The future of the European Union will also shape the EFTA’s fate because of the latter’s heavy reliance on exports to EU countries. Any new crises to arise in the eurozone would likely damage the economies of Switzerland, Norway, Iceland and Liechtenstein as well. The EFTA will thus have to diversify its export markets as much as it can to hedge against risk to the Continental currency area. Some of the bloc’s members, however, will struggle to diversify their own economies: Iceland is still dependent on certain industries such as fish and aluminum production, making it vulnerable to volatility in those sectors. Switzerland and Liechtenstein, meanwhile, have come under mounting international pressure to introduce greater transparency to their banking sectors.

Because the EFTA’s members boast highly developed and diversified industrial bases, the bloc is eager to gain tariff-free access to the industrial sectors of its trade partners. The organization’s primary exports include chemicals, pharmaceutical products, oil and machinery. In addition to being the third-largest oil producer in the world, Norway has a large fisheries sector to promote, as does Iceland. Metals are also important to the bloc: Switzerland is a leading refiner of gold; Norway is a major exporter of aluminum, iron and steel, magnesium, nickel, and zinc; and Iceland is a significant aluminum producer.

Given the notable high-tech companies that EFTA members house, the bloc tends to emphasize intellectual property rights during its free trade negotiations. The organization has done its best to include measures that enforce its members’ rights against infringement, counterfeiting and piracy in its deals, as well as provisions on data protection. This issue is especially important to Switzerland, which hopes to protect the patents of its pharmaceutical and biotechnology industries. It’s no coincidence that the Berne Convention — one of the foundational international accords on copyright protection — was signed in Switzerland in 1886.

Defensive Interests

The European Economic Area principle of the free movement of goods doesn’t apply to trade in agricultural products. And unlike the European Union, the EFTA does not have a common agricultural policy. As a result, its members have enacted some of the highest farming subsidies in the world, with tariffs averaging 40 percent — four times larger than the EU average. When the EFTA negotiates free trade agreements, it generally reserves basic products such as sugar and grain for bilateral arrangements between individual member states and the partner country in question. By contrast, the bloc tends to settle deals on processed food products, such as chocolate, as a whole.

Fisheries are an equally sensitive subject. In fact, the EFTA’s desire to protect its agricultural and fisheries industries is one of the primary obstacles to its members’ ascension to the European Union, and none participate in the EU Common Fisheries policy. Norweigian voters have twice rejected EU membership for fear the Continental bloc would threaten the all-important sectors. Iceland likewise withdrew its EU membership request over concerns about fishing quotas and regulation.

Immigration is a source of concern for the EFTA as well. Because of their membership in the European Economic Area, Norway, Iceland and Liechtenstein have had to agree to permit the free movement of EU workers across their borders. However, this membership also includes a “safeguard measure” that allows countries to temporarily restrict migration in the face of serious “economic, societal or environmental difficulties.” Switzerland’s handling of EU migrants, meanwhile, is dictated by its bilateral agreement with the bloc. The Swiss population opted in 2014 to introduce a quota on EU migrants, endangering the country’s deal with Brussels. After two years of negotiation, the government in Bern abandoned the controversial quota plan, choosing instead to limit immigration by giving its citizens priority in filling new jobs.